아랍에미리트(UAE)에서는 지역별 불확실성이 소비자들에게 일률적인 반응을 이끌어내지 못하고 있다. 오히려 Numerator가 Worldpanel을 통해 실시한 새로운 전국 조사 결과에 따르면, 가구들은 세 가지 뚜렷한 심리로 나뉘어 있으며, 각 그룹은 소비 패턴, 우선순위, 그리고 신뢰도를 서로 다른 방식으로 재편하고 있는 것으로 나타났다.

1,294명의 주 구매자를 대상으로 실시한 설문조사 결과에 따르면, 가정이 비용 부담, 안정성, 미래에 대해 느끼는 인식이 이제 실제 재정 상황만큼이나 중요해졌다는 사실이 밝혀졌습니다. 이 세 가지 요소가 결합되어, 각 카테고리별로 가치, 충성도, 성장세가 왜 이렇게 다른 양상을 보이는지 설명해 줍니다.

“이 가구들은 서로 다른 방향으로 나아가고 있습니다.”라고 Numerator Africa & Middle East 산하 Worldpanel의 고급 분석 부문 솔루션 디렉터인 카란 굽타(Karan Gupta)는 말합니다. “브랜드는 더 이상 가치에 대한 단일한 정의에만 의존할 수 없습니다. 관련성은 서로 다른 가족들이 동일한 환경에 대해 감정적, 재정적으로 어떻게 반응하고 있는지를 이해하는 데 달려 있습니다.”

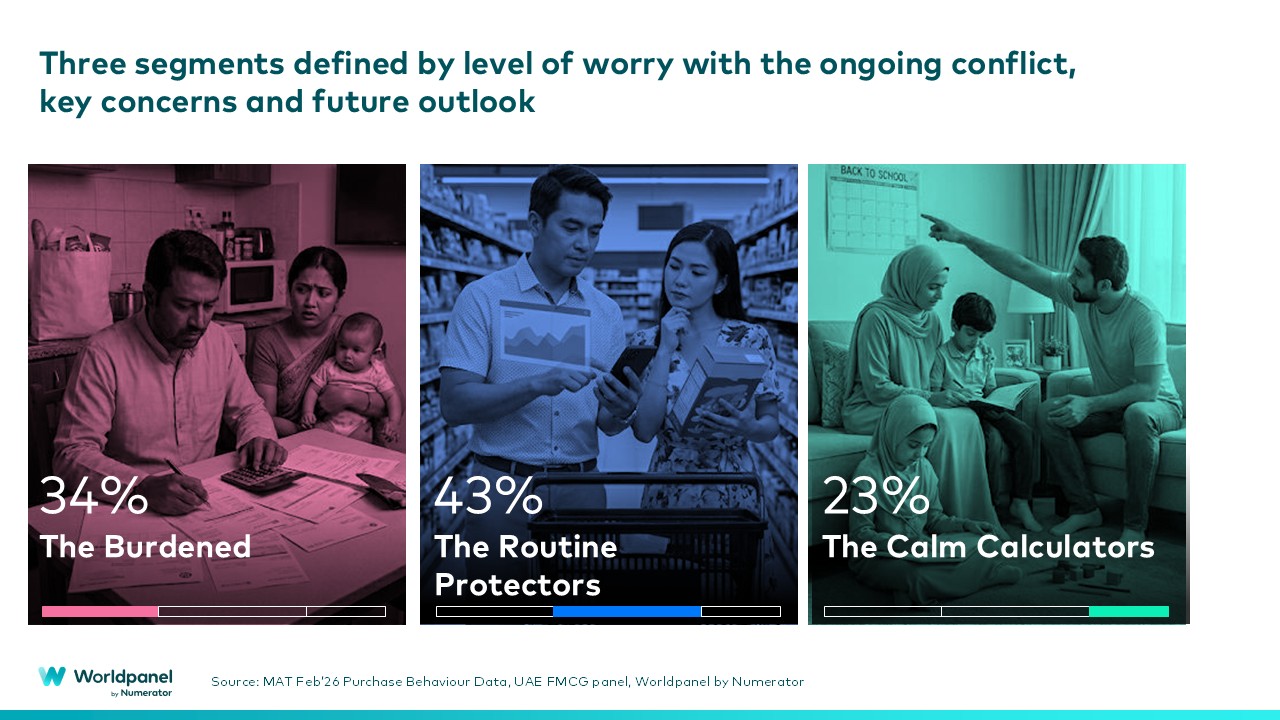

부담감을 느끼는 사람들 (34%) – 신중하고, 제약을 받으며, 소극적인 태도를 보임

가장 큰 부담 요인은 UAE 가구의 3분의 1을 약간 넘는 비중을 차지하는 ‘부담감에 시달리는 계층’에서 비롯됩니다. 이 그룹은 전반적인 여건과 자신의 재정 전망 모두에 대해 가장 비관적인 태도를 보이고 있습니다.

생활비 상승, 소득 안정, 가족의 안전에 대한 우려가 이들의 주된 고민거리로 떠오르면서, 일상적인 지출은 물론 장기적인 지출까지 눈에 띄게 줄고 있다. 응답자의 10명 중 8명에 가까운 사람들이 향후 6~12개월 동안 UAE 내 자산에 투자할 의향이 없다고 답했는데, 이는 당장의 필요를 넘어서는 부분에 대한 신뢰도가 낮음을 시사한다.

압박을 받으면 브랜드 충성도는 쉽게 흔들립니다. 선호하는 식료품 브랜드를 구할 수 없거나 가격이 너무 비싸지면 상당수의 소비자가 더 저렴한 제품으로 갈아타려는 경향이 있어, 가격의 결정적 요인으로서의 중요성이 더욱 커지고 있습니다.

‘일상의 수호자’(43%) – 안정과 가족의 안녕을 지키는 이들

반대편 끝에는 가장 큰 비중을 차지하는 그룹인 ‘일상 수호자’가 자리 잡고 있으며, 이들은 전체 가구의 43%를 차지합니다. 이 그룹은 경제적 제약은 상대적으로 적지만, 감정적 요인에 크게 좌우되는 경향이 있습니다.

이들의 관심사는 단순히 재정적인 문제보다는 가족의 안녕, 아이들의 일상, 그리고 정신적 안정을 지키는 데 집중되어 있습니다. 이들은 소비를 완전히 중단하는 것은 아니지만, 실험이나 확장에 앞서 지속성과 통제력을 우선시하며 더욱 신중하게 선택하고 있습니다.

이러한 사고방식은 익숙한 브랜드와 예측 가능한 형식을 선호하고, 특히 가정 내 소비와 같은 일상적인 습관을 뒷받침하는 구매 행태로 나타납니다.

‘침착한 계산가들’(23%) – 회복력은 뛰어나지만 매우 신중한 편

가장 작은 집단인 ‘침착한 계산가들’은 정서적 회복력과 비교적 낙관적인 태도로 두드러집니다. 재정적으로 자신감이 있는 이들은 여전히 시장에 관심을 가지고 있지만, 지출에 있어서는 훨씬 더 신중한 태도를 보입니다.

이 그룹은 물가와 경제 지표를 면밀히 주시하며, 구매를 신중하게 검토하고 지출처와 방식을 적극적으로 최적화하고 있습니다. 이들은 소비를 아예 줄이는 대신, 효율성과 현명한 가치, 장기적인 이익을 중시하며 소비 패턴을 세심하게 다듬고 있습니다.

평균이 아닌 편차가 만들어낸 시장

이 세 가지 부문은 종합적으로 UAE 시장의 중대한 변화를 여실히 보여줍니다. 소비자들은 단순히 ‘저가 제품으로 전환’하거나 ‘현 상태를 유지하는’ 데 그치지 않습니다. 그들은 정서적, 행동적, 재정적 측면에서 각기 다른 방향으로 나아감으로써, 일률적인 전략으로는 대응하기 어려운 상황을 만들어내고 있습니다.

이번 시리즈의 두 번째 기사에서는 이러한 사고방식이 이미 FMCG 업계 전반에 걸쳐 일상 생활 패턴, 라마단 기간 중의 행동 양상, 카테고리별 취약성 및 브랜드 리스크에 어떤 변화를 가져오고 있는지 살펴봅니다.

이번 설문조사 결과와 그 결과가 귀사의 브랜드 및 카테고리에 어떤 의미를 지니는지 미리 확인하고 싶으시다면, 당사의 현지 전문가에게 문의해 주십시오.

카란 굽타 (Karan Gupta)

고급 분석 솔루션디렉터

Numerator Africa & Middle East의 Worldpanel

.svg)